This practice ensures any errors or fraudulent activities are caught early. Begin by aligning the bank account balance with the cash balance on your company’s balance sheet. Check if the bank deposits and withdrawals match the records on the balance sheet. If there are any differences between the bank statement and the balance sheet, cross-check to identify the mistake’s source.

Double Entry Bookkeeping

(b) Checks Nos. 789 and 791 for $5,890 and $920, respectively, do not appear on the bank statement, meaning these had not been presented for payment to the bank by 31 May. Banks often record other decreases or increases to accounts and notify the depositor by mailed notices. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting.

Do you own a business?

If you want to prepare a bank reconciliation statement using either of these approaches, you can use the balance as per the cash book or balance as per the passbook as your starting point. These fees are charged to who should prepare a bank reconciliation? your account directly, and reduce the reflected bank balance in your bank statement. These charges won’t be recorded by your business until your bank provides you with the bank statement at the end of every month.

Bank Reconciliation Accounting

Many companies may choose to do additional bank reconciliations in situations that involve large sums of money or that show unusual financial activity. This can include large payments and deposits or notifications of suspicious activity from your bank. In these situations, it’s a good idea to perform an immediate reconciliation. By comparing your company’s internal accounting records to your bank statement balance, you can confirm that your records are accurate and analyze the reasons behind any potential discrepancies. Reconciling your bank statement used to involve using a checkbook ledger or a pen and paper, but modern technology—apps and accounting software—has provided easier and faster ways to get the job done.

Identify errors with check deposits

It’s imperative to maintain detailed sets of records of the current reconciliation process and any adjustments made. Each step of the reconciliation process should be clearly recorded, including any discrepancies found and the actions taken to resolve them. This practice not only aids in internal reviews but also provides an audit trail. Financial statements show the health of a company or entity for a specific period or point in time.

- But this is not the case as the bank does not clear an NFS check, and as a result, the cash on hand balance gets reduced.

- Regular bank reconciliation saves you from having to review a full year of financial records—instead, you can quickly consult your reconciliation statements to review any required information.

- Begin with a side-by-side comparison of your bank account statement and your company’s accounting records.

- This practice is essential for maintaining the financial health and integrity of your business.

Automate the process

These reconciliations typically involve live transaction matching between an accounting system and a live feed from a financial institution, and reduce the risk of errors and fraud. Sheetgo is a powerful automation tool that can significantly streamline the bank reconciliation process. Its Finance solution includes a bank reconciliation module which automates the comparison of financial records with bank statements.

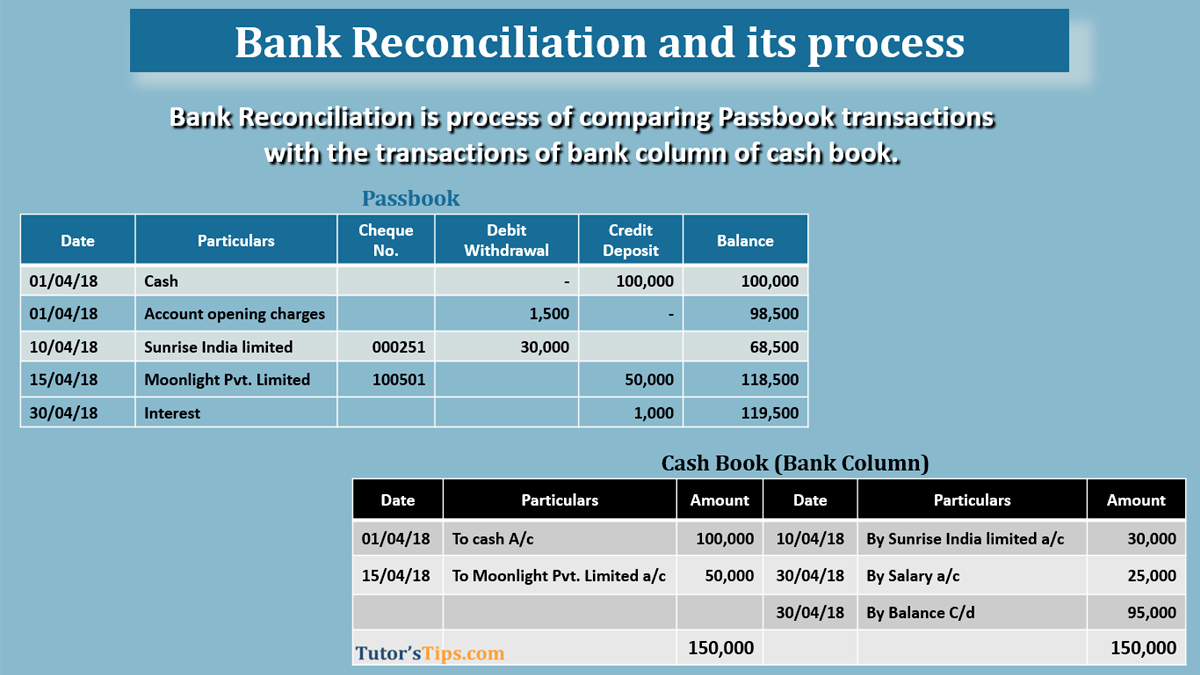

A bank reconciliation statement is a document that is created by the bank and must be used to record all changes between your bank account and your accounting records. It shows what transactions have cleared on your statement with the corresponding transaction listed in your journal. Your bank may collect interest and dividends on your behalf and credit such an amount to your bank account. Nowadays, all deposits and withdrawals undertaken by a customer are recorded by both the bank and the customer. The bank records all transactions in a bank statement, also known as passbook, while the customer records all their bank transactions in a cash book.

Compare the business’s financial records to the bank statement to spot the errors. This can be accomplished by matching transactions, and then adding or deducting any transactions that do not align to balance the total amounts. Outstanding checks are those that have been written and recorded in the financial records of the business but have not yet cleared the bank account. This often happens when the checks are written in the last few days of the month. The more frequently you do a bank reconciliation, the easier it is to catch any errors.

This can happen if you’re reconciling an account for the first time or if it wasn’t properly reconciled last month. You should perform monthly bank reconciliations so you can better manage your cash flow and understand your true cash position. Read on to learn about bank reconciliations, use cases, and common errors to look for. Bank reconciliation isn’t just important for maintaining accurate business finances—it also ensures your customer and business relationships remain strong.

Then when you do your bank reconciliation a month later, you realize that cheque never came, and the money isn’t in your books (even though your bookkeeping shows you got paid). Reconciling your bank statements lets you see the relationship between when money enters your business and when it enters your bank account, and plan how you collect and spend money accordingly. Any credit cards, PayPal accounts, or other accounts with business transactions should be reconciled. It’s important to perform a bank reconciliation periodically to identify fraudulent activities or bookkeeping and accounting errors. This way, you can ensure your business is in solid standing and never be caught off-guard. If your beginning balance in your accounting software isn’t correct, the bank account won’t reconcile.

This process ensures accurate tracking of financial transactions and balances. Bank reconciliation is the process of comparing accounting records to a bank statement to identify differences and make adjustments or corrections. In the case of personal bank accounts, like checking accounts, this is the process of comparing your monthly bank statement against your personal records to make sure they match. Many banks allow you to opt for fee-free electronic bank statements delivered to your email, but your bank may mail paper bank statements for a fee. In the bank reconciliation process, the total amount of outstanding checks is subtracted from the ending balance on the bank statement when computing the adjusted bank balance.